Creating an effective cash flow management system begins with forecasting and analysis. By understanding your current cash usage and identifying potential shortfalls, you can develop policies and procedures to maintain adequate liquidity.

What is cash flow?

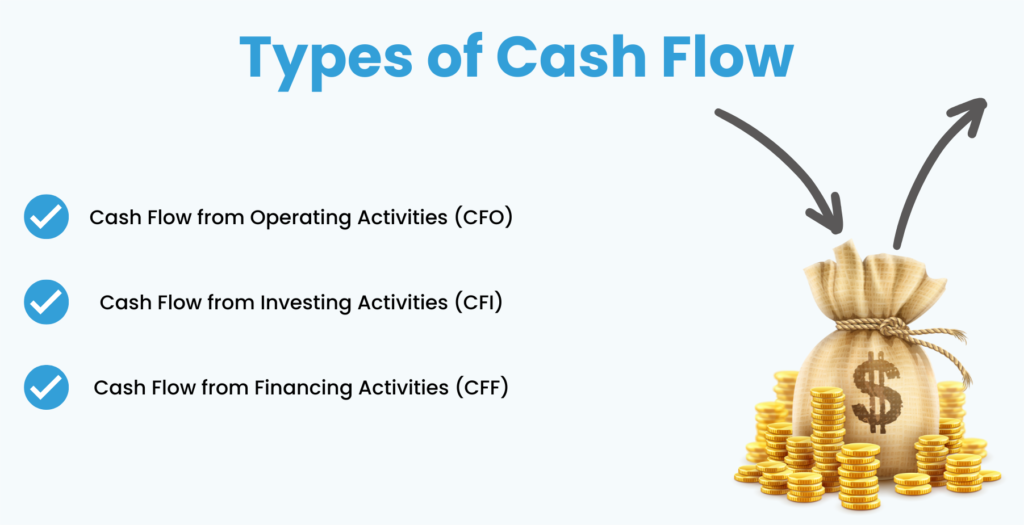

Cash flow refers to the movement of cash in and out of a business or individual over a specific period. It represents the net amount of cash generated or used during that time. There are three main types of cash flow that financial professionals and business owners analyze:

Here are some steps to help you manage cash flow

Step 1: Determine your cash flow cycle

Start by mapping out your company’s cash flow cycle. This involves defining how long it takes to generate cash from your daily activities, including the time needed to:

- Purchase parts or supplies

- Manufacture products

- Receive payment for sold products or services

A shorter cash flow cycle means you have more money available to pay bills and restart the cycle. Frequent cash flow cycles indicate higher efficiency, as you can quickly gain returns on your operations.

Step 2: Increase the cash you generate per cycle

If you fall short of cash within each cycle, you may need to find ways to increase cash receipts from sales to generate positive cash flow. Consider these strategies:

- Raise sales volume

- Create larger profit margins

- Reduce expenses and salaries

- Speed up operational processes to generate more cash flow cycles annually

Step 3: Ensure you have enough time and resources

While your passion and conviction are vital for promoting your business, spending all your time trying to generate cash—such as applying for loans or seeking investors—can cause you to miss other opportunities for sales and marketing. Ensure your business has the right resources to manage cash flow and handle other essential tasks for success.

By following these steps, you can effectively manage your cash flow, ensuring your business remains financially healthy and capable of seizing growth opportunities.

How do cash flow problems usually start?

Cash flow problems often start for several common reasons:

- Poor sales: If a business isn’t making enough sales, it won’t bring in enough cash to cover its expenses.

- Late payments from customers: When customers delay payments, it disrupts the business’s cash flow, making it hard to pay bills on time.

- High overhead costs: Excessive expenses, such as rent, utilities, and salaries, can drain cash reserves quickly.

- Overstocking inventory: Holding too much inventory ties up cash that could be used elsewhere in the business.

- Rapid growth: Expanding too quickly without adequate planning can lead to a cash crunch, as more money is needed to fund the growth.

- Unexpected expenses: Unplanned costs, like equipment breakdowns or emergency repairs, can suddenly deplete cash reserves.

How to avoid cash flow problems?

To prevent cash flow issues, businesses can take several proactive steps:

- Forecast cash flow: Regularly forecast your cash flow to predict future cash needs and identify potential shortfalls early.

- Monitor receivables and payables: Maintain a clear picture of both accounts receivable (money owed to you by customers) and accounts payable (money you owe to vendors). Follow up promptly on late payments from customers and consider offering discounts for early payments to incentivize faster settlements.

- Manage inventory: Avoid overstocking by maintaining an optimal level of inventory. Use just-in-time inventory practices if possible.

- Control expenses: Regularly review your expenses and cut unnecessary costs. Negotiate better terms with suppliers to reduce overhead.

- Plan for growth: When planning to grow, ensure you have a solid financial plan that includes adequate cash reserves to support expansion.

- Maintain a cash reserve: Set aside a portion of your earnings as a cash reserve to cover unexpected expenses or downturns in sales.

- Use financing wisely: Use lines of credit or loans to cover short-term cash needs, but be cautious of taking on too much debt.

- Improve sales strategies: Increase your sales efforts through effective marketing and promotions to boost revenue.

- Review pricing: Ensure your pricing covers costs and generates a profit. Regularly review and adjust prices as needed.

By following these steps, businesses can better manage their cash flow, ensuring they have enough liquidity to operate smoothly and avoid financial difficulties.

Strategies for effective cash flow management

Ever feel like you’re waiting forever for customer payments? It can be a real drag on your business cash flow. But fear not, there are ways to fix this!

If those invoices are piling up, here are some simple things you can try:

- Revamp your billing: Take a look at how you send out bills. Can you change it to better match your income flow? For example, could you offer monthly plans instead of individual bills for smaller jobs?

- Pick the right customers: Do a quick check before working with someone new. This can help you avoid customers who might be slow to pay.

- Auto-pilot invoicing: There’s cool software that can send invoices automatically! These can even send reminders if a payment is late.

- Set up auto-billing: For regular customers, like those on retainer plans, see if they’d be okay with automatic payments. This is a great way to get paid on time, every time!

- Bill more often: Think about sending bills more frequently. Instead of waiting a month, could you send them every two weeks? More frequent bills mean more frequent payments!

- Get a down payment: For big projects or long contracts, ask for a deposit upfront. This shows the customer’s commitment and gives you a cash cushion. You can even split the remaining balance into progress payments.

- Mobile payments: There are handy apps that let you accept payments with your phone! This is a super convenient way to get paid on the spot, no matter where you are.

Keep a cash flow forecast

A cash flow forecast is like your own personal financial weather report, helping you plan for the next 6 to 12 months.

Why forecast?

- Plan for growth: Set realistic growth goals without putting your cash flow at risk.

- Prepare for seasonal Swings: Is your business busier during holidays? Knowing this helps you plan for potential dips in income during slower months.

- Manage expenses: Identify upcoming fixed costs (rent, salaries) and variable costs (inventory, marketing) to ensure you have enough cash on hand.

Building your forecast

- Timeframe: Look 6-12 months ahead. Break it down further (monthly or quarterly) if needed.

- Sales: Project your expected sales for each period. Consider historical data, seasonal trends, and any marketing campaigns you plan.

- Fixed Costs: List all expenses that stay the same each month (rent, utilities, loan payments).

- Variable Costs: Estimate expenses that fluctuate (inventory purchases, shipping costs, commissions). Base these on your sales projections.

- Other Income: Include any income outside of sales (interest, investments).

Putting it all together

For each period, subtract your total expenses (fixed + variable) from your income (sales + other income). This will show you your projected net cash flow – positive means you have extra cash, negative means you might need a cash injection (loan, savings).

How to increase cash flow?

While strong sales and effective cash management help improve cash flow, additional strategies can further ensure sufficient liquidity. Here are some simple techniques:

Schedule bill payments strategically

- Carefully check supplier invoices to determine exact due dates.

- Create a schedule to delay payments as long as possible without missing discounts.

Switch to electronic invoicing

- Adopt electronic invoicing and payments to cut down on paper and printing costs.

- Electronic transactions are faster than traditional mail, and the initial investment in technology can be recouped over time.

Maintain an emergency cash reserve

- Like personal savings, keep a certain amount of cash available for emergencies.

- Ensure you have enough liquidity but avoid hoarding cash that could be used for profitable investments. Follow industry guidelines for cash reserves.

Conduct detailed cash flow analysis

- Use cash flow statements to track how cash moves in and out of the business.

- Keep a detailed cash journal to monitor transactions closely, and review these reports to understand spending patterns.

Reconcile accounts regularly

- Regularly match your cash balances with bank statements to identify discrepancies.

- Investigate any differences and separate the tasks of handling cash and recording transactions to prevent fraud.

Enforce payment terms with customers

- Ensure customers pay on time to maintain a healthy cash flow.

- Promptly follow up with late-paying customers and enforce the terms of late payments in contracts to avoid disruptions in paying your vendors.

Bottom line

By implementing the strategies outlined in this blog post, you can take control of your cash flow and ensure your business thrives. However, managing cash flow effectively can be time-consuming, and that’s where Bookkeeperlive comes in.

Our expert bookkeepers can:

- Streamline your record-keeping: Free yourself from tedious data entry and focus on running your business.

- Forecast cash flow with pinpoint accuracy: Gain insights into your financial future and make informed decisions.

- Identify areas to optimize your finances: We’ll uncover hidden opportunities to improve your cash flow.

With Bookkeeperlive by your side, you’ll gain the peace of mind that comes with knowing your cash flow is under control, allowing you to focus on what you do best – running a successful business!

FAQs

1. What’s the difference between cash flow and profit?

A: Profit is the money remaining after all your expenses are paid for a specific period. Cash flow, on the other hand, refers to the actual movement of money in and out of your business during that time. You can have a profit on paper but still struggle with cash flow if customer payments are slow or expenses are due before you receive income.

2. When should I seek professional help with cash flow management?

If you’re struggling to manage your cash flow on your own, consider seeking help from a financial advisor or bookkeeper. They can provide expert guidance, develop customized strategies, and help you implement best practices for improved financial health.

3. I understand the cash flow cycle, but how can I analyze it for better insights?

A: Analyzing your cash flow cycle involves calculating key metrics like cash conversion cycle (time it takes to convert inventory into cash) and average payment collection period (average time it takes customers to pay invoices). These metrics can help identify areas for improvement, such as speeding up collections or optimizing inventory levels.

4. I’m a seasonal business. How can I manage cash flow during slow periods?

A: Seasonal businesses can benefit from building a cash reserve during peak seasons to cover expenses during slower periods. Additionally, explore options like offering pre-season discounts or subscriptions to encourage early purchases and generate cash flow in advance.

5. How can I prevent cash flow problems before they happen?

A: The key is proactive management. Regularly review your budget and cash flow forecast, monitor accounts receivable and payable closely, and be prepared to adjust your strategies as needed. Building a healthy cash reserve can also act as a buffer during unexpected situations.