In 2023, 23% of small business owners consider inflation as their second most significant concern, following the quality of labor, which stands at 24%. Interestingly, taxes, a recurring issue at the end of every financial year, rank as the third most pressing problem for US small businesses, with 17% acknowledging its importance.

Running a retail business can be incredibly rewarding, but it also comes with its fair share of challenges. One of those challenges is managing your finances and dealing with taxes. If you’re a small business owner, it’s essential to understand how taxes impact your business and to have a plan in place to ensure stress-free accounting for retail businesses. In this blog, we’ll explore how taxes affect your growing retail business, provide you with valuable small business tax tips, and delve into key aspects of retail accounting, including inventory management and the accounting cycle.

How taxes impact your business

Taxes can have a significant impact on your retail business. Here’s how they affect you and what you need to know:

1. Business structure matters

Your business’s legal structure (e.g., sole proprietorship, partnership, or corporation) significantly impacts your tax liability. Each structure comes with varying tax rules and rates. It’s essential to select the right structure for your business to minimise your tax burden and consider retail accounting services. Consulting with a tax professional can assist you in making the correct choice.

2. Sales tax

If your retail business sells physical products, you’ll likely have to collect sales tax from your customers, a critical aspect of retail tax preparation service. This tax must be reported and remitted to the appropriate authorities. Failing to do so can result in penalties and fines.

3. Income tax

You’ll also need to pay income tax on the profits your retail business generates. Accurately tracking your income and expenses is vital to determine your taxable income. Deductions, such as business expenses and depreciation, can help lower your tax liability.

4. Employment taxes

If you have employees, you’ll be responsible for payroll taxes, which include Social Security, Medicare, and federal income tax withholding. Managing these taxes correctly is crucial to avoid compliance issues.

5. Tax credits

Be aware of tax credits and deductions available to small businesses. For instance, the Small Business Health Care Tax Credit can help you cover employee health insurance costs. Research available tax incentives to take advantage of these opportunities.

6. State and local taxes

In addition to federal taxes, it’s essential to consider that state and local taxes can also significantly impact your business, especially in industries like grocery store accounting. These local taxes may encompass state income tax, property tax, and local sales taxes. Understanding and complying with your local tax obligations is just as critical as managing federal taxes.

Small business tax tips for retail business

Now, let’s dive into some practical tips to help you manage your retail business’s taxes more effectively:

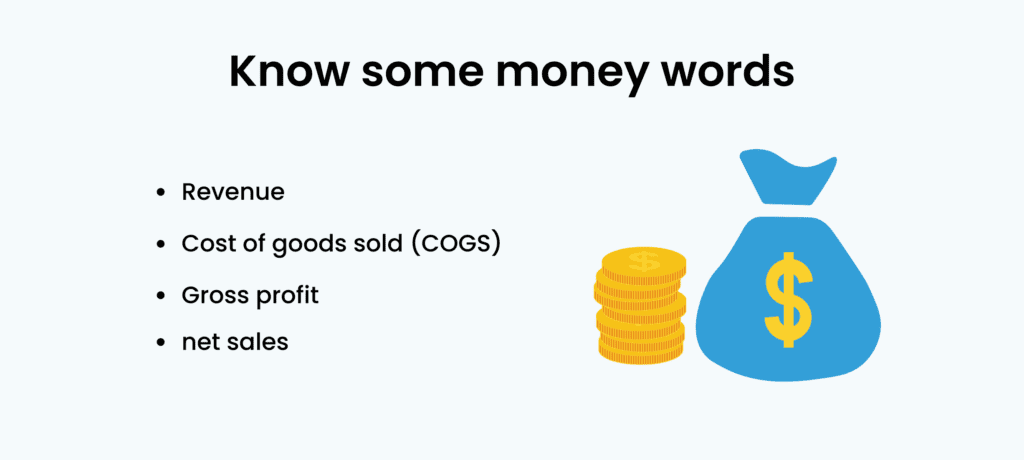

1. Understand financial words

Revenue: This is how much money you make from selling stuff.

Cost of goods sold (COGS): It’s how much it costs to make the stuff you sell.

Gross profit: This is what’s left after taking away COGS from what you earn.

Net sales: The money you make after paying all your bills.

2. Keep business and personal money separate

The initial step to take when launching a small business involves establishing a dedicated business bank account.

Maintaining separate bank accounts for your business and personal finances simplifies the process during tax season. This practice ensures that you maintain precise and organized records for deductible expenses, while also safeguarding the privacy of your personal transactions.

3. Keep good records

Have clean and correct records. When tax time comes, it’s much easier if your papers are tidy. Look at your bank statements and compare them to your receipts and bills.

5. Watch your inventory

Keep track of how much stuff you have to sell. This is important for taxes. It’s best to use a good computer program for this, like QuickBooks, Zoho Books, or Xero.

6. Save for retirement

Many small business owners think they’re in control of their financial future. You can prepare for it and get a tax benefit by putting some of your business profits into your own 401(k) savings account.

This idea also works for your store employees. Giving money to their retirement savings is a good perk for some retail workers. And the best part is, the money you put in is tax-deductible, which is good for everyone.

7. Use section 179

If you’ve bought costly equipment during the year, such as top-notch lighting systems or store security cameras, take advantage of the Section 179 tax deduction. This lets you deduct the entire purchase price from your taxes, which can lower what you owe.

But remember, there are some specific rules for claiming Section 179. The equipment must be used for business purposes for over 50% of the time, actively used in the current financial year, and you must have bought it outright. Plus, there’s a limit of $1.08 million on the amount you can deduct.

8. Use bonus depreciation

You can also lower your taxes by using bonus depreciation when you buy expensive stuff for your business. It’s a bit different than Section 179.

9. Get ready for tax time

Tax time can be a headache, but it doesn’t have to be. Get your money organized before tax time comes. There are two important dates to keep in mind:

March 15: If your business is an S corporation or partnership.

April 15: For personal tax returns or single-member LLCs.

3 Methods for retail accounting inventory expense calculation

Inventory is a critical aspect of retail accounting. There are three common methods for accounting for inventory costs: FIFO (First-In, First-Out), LIFO (Last-In, First-Out), and Weighted Average. Each method has its advantages and disadvantages, and your choice can impact your financial statements and tax liability. Consult with an accountant to determine the best method for your business.

1. FIFO (first-in, first-out)

Imagine your inventory as a line of products on a shelf. With the FIFO method, you assume that the first items you put on the shelf are the first ones to be sold. It’s like serving the customers who arrived first in a queue. So, when you calculate your inventory costs and the value of products you’ve sold, you consider the oldest items as being sold first.

Advantages

It often reflects the actual flow of inventory in many retail businesses.

This can result in lower taxable income, which means you pay less in taxes.

Disadvantages

During rising prices, it can make your profits look higher on paper because you’re selling older, cheaper inventory first.

2. LIFO (last-in, first-out)

Now, picture your inventory shelf again, but with the LIFO method, you assume that the last items you put on the shelf are the first ones to be sold. It’s like serving the customers who arrived last in a queue. So, when calculating your inventory costs, you consider the newest items as being sold first.

Advantages

During rising prices, it can lower your taxable income, reducing your tax bill.

Disadvantages

It might not represent the actual flow of inventory in your business, making it less practical for some retailers.

Can make your profits appear lower on paper, which could affect your ability to secure loans or investments.

3. Weighted average

Think of the weighted average as taking the average cost of all the items on your shelf. You add up the total cost of all the items and then divide it by the total number of items to find the average cost per item. When you sell products, you use this average cost to calculate your inventory expenses.

Advantages

It’s simple to use and doesn’t fluctuate as much with changing prices.

It can be a good middle ground between FIFO and LIFO, suitable for many businesses.

Disadvantages

It might not perfectly match the actual cost of the items you sell, especially if your inventory costs vary widely.

Choosing the right method for your business depends on various factors, including the type of products you sell, price trends, and tax implications. Consulting with an accountant for your retail store bookkeeping and tax preparation is a smart move because they can help you decide which method works best for your specific situation.

How can I monitor my current inventory?

Accurate inventory tracking is crucial for retail businesses. Implement a reliable inventory management system, use barcoding or RFID technology, and conduct regular physical counts to ensure your on-hand inventory matches your records. This not only helps with financial accuracy but also minimizes the risk of overstocking or running out of products.

The accounting cycle for retail stores

The accounting cycle for retail stores involves several steps: recording transactions, journalizing, posting to the general ledger, preparing trial balances, making adjusting entries, creating financial statements, and closing the books. This cycle helps maintain financial accuracy, track profits and losses, and comply with tax regulations. It’s essential to follow this cycle meticulously for effective financial management.

Conclusion

By following the steps outlined in this guide, you can ensure that your financial management is not just smooth, but also hassle-free. Taking the time to get your finances organized and seeking professional guidance when needed are key to your business’s success. With the right approach, you can focus on growing your retail business and worry less about tax-related stress and financial inaccuracies. Remember, a strong financial foundation is essential for the long-term success of your business.

At BookkeeperLive, we’re here to help you with bookkeeping for small retail businesses. Our expert team can assist you in managing your finances efficiently. If you have any doubts or need guidance, don’t hesitate to reach out to our experts. We’re offering a free trial so you can experience the benefits of our services firsthand. Let us be your trusted partner in achieving financial success for your retail store.