If you often find yourself missing deadlines and haven’t filed your taxes or maintained financial records for a while. Don’t worry, we have got you covered. As a small business owner or a financial person with hundreds of tasks, it is a good practice to maintain clean historical bookkeeping records. Bookkeeperlive bookkeeping services will help you in accurate tax filing, ensuring compliance, and driving financial decisions for better business growth.

Historical bookkeeping is like digging into financial history and then finding all the unclear records. It will enable you to record and organize bank statements, receipts, and bills by date. You will better understand exactly where your money went. This gives you a thorough knowledge of filing taxes. Good records help you report all income and find expenses you can deduct. You'll make fewer mistakes and avoid problems with the IRS. Most importantly, it brings peace of mind. You can stop worrying about unfiled taxes and get back on track with tax laws.

The key benefits of implementing historical bookkeeping include the following:

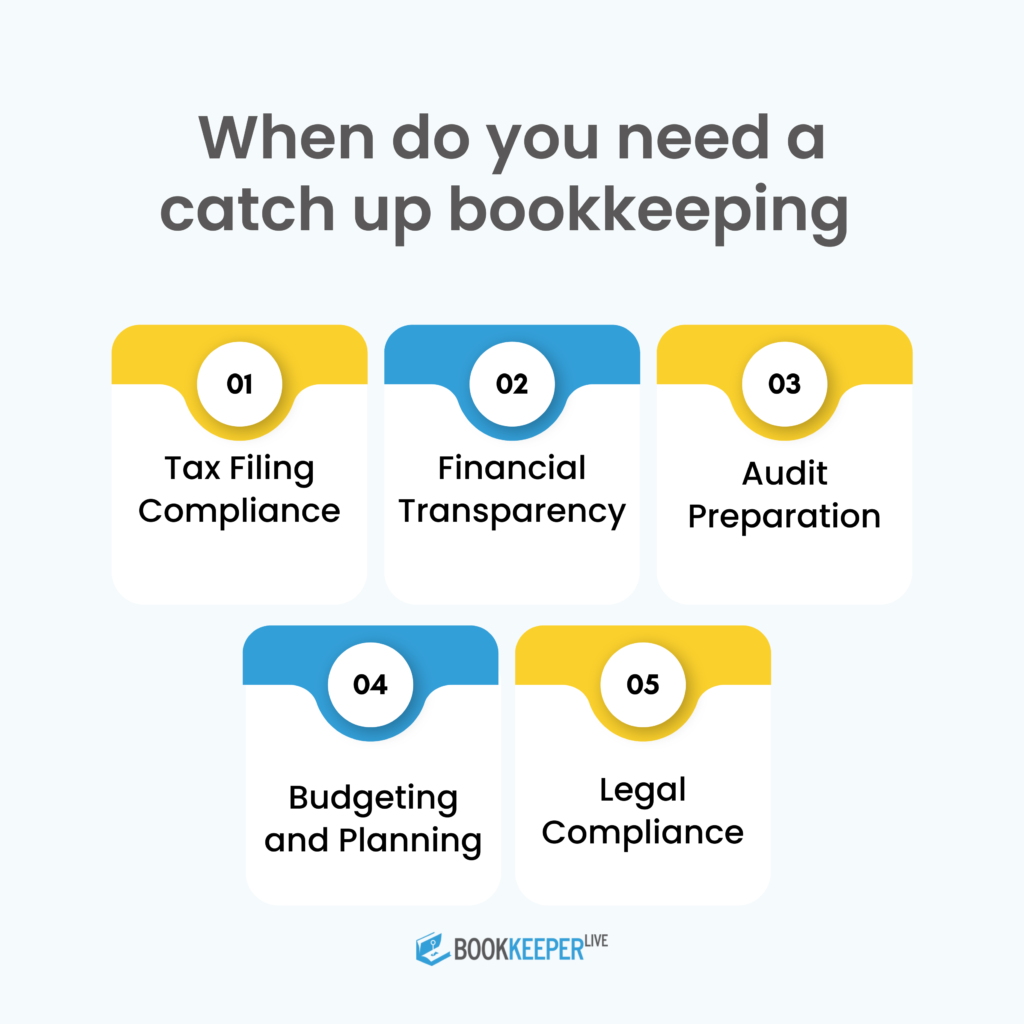

Meeting IRS requirements: The IRS says businesses must keep detailed records of money coming in and going out. This helps make sure your tax returns are accurate.

More than just receipts: You need more than just receipts and bank statements. You also need a clear list of all the transactions your business made.

Audit Protection: Good records will make processes easier and quicker during audits. It helps you stay prepared wth no missing recipients and bills. Sorting this out will save yourself from an explanation.

Good Records: Good bookkeeping gives you a well-organized list of how much money your business made and spent. This makes it easier to figure out how much of your money the IRS can tax when you file old tax returns.

Get All Your Deductions: Every business expense you can deduct reduces your taxable income. Good bookkeeping tracks all eligible deductions like travel costs and office supplies.

Avoid CP2566 Problems: When you don't file, the IRS might send a CP2566 Notice demanding payment based on income estimates. They won't include your deductions, which means a bigger bill.

Prevent Substitute Returns: If you keep ignoring taxes, the IRS might file a Substitute for Return (SFR) for you. This only counts income from W-2s and 1099s. It ignores deductions, which can make your tax bill much higher.

Don't Miss Refunds: Even profitable businesses sometimes get refunds through deductions. An SFR without deductions might show you owe money instead of getting money back.

Use Records to Negotiate: Good bookkeeping tracks your deductions. You can use these records to negotiate a fair tax bill with the IRS, even after they file an SFR.

It is easy to fall behind on your books. Maybe you got busy. Maybe you didn’t have help. It happens. The good news is you can get back on track. Here’s how.

Pull together everything. Get bank statements, invoices, receipts, loan papers, and tax forms. If you can’t find something, ask your bank or vendors for copies.

Put papers and files in order. Start with the oldest year. Break it down month by month. This helps you see what you have and what’s missing.

Check your statements against what’s in your books. If you don’t have records yet, use the bank statements to rebuild them. Make sure every deposit and payment makes sense.

Log all money in and out. Use simple software or a spreadsheet. Put each amount in the right spot like sales, supplies, rent, or wages.

Match what customers paid with what you billed them. Do the same for bills you paid. Look for anything unpaid or paid twice. Fix any errors.

If you pay staff, check your pay records. Make sure you paid the right tax and filed on time. If something’s off, fix it now.

Look for wrong numbers or missing entries. Fix them before you close each month. It’s better to catch mistakes early.

Once each month looks right, close it out. Reconcile your accounts. Keep copies of reports. Good records make tax time easier.

Once you’re caught up, stay on top of it. Update your books every week. Use software to make it easy. If you’re short on time, pay someone to do it.

If you are still struggling to manage your historical bookkeeping, consider hiring a professional from Bookkeeperlive. Historical bookkeeping can be overwhelming, especially if you are handling multiple roles in your business. At BookkeeperLive, we will take care of years of uncleared records,s ensuring accuracy and efficiency. We assist you in IRS audit and examination. From discovering errors in past tax filing to improving financial decision-making, we assist you in every step.

1. How historical bookkeeping is it different from regular bookkeeping?

A: Regular bookkeeping focuses on current transactions as they happen. Historical bookkeeping involves organising, analyzing, and maintaining records from past periods - whether that's last month, last year, or several years back.

2. How long should I keep historical financial records?

A: Most of the

3. How should I organize historical records?

A: Create a system with:

Consistent Naming: Use formats like "YYYY-MM-DD_Amount_Vendor_Category"

4. What if I've lost important historical records?

A: You can often recover them:

5: How do I handle missing receipts for tax deductions?

A: Options include:

6: Can poor historical bookkeeping affect my credit score?

A: yes, it can affect your credit score in the following areas:

7: As a small business owner, what historical records are most critical?

A: Priority records include:

8: How do I separate personal and business historical records?

A: Maintain completely separate systems:

Make Historical Bookkeeping a Success

Keep track of all of your earnings and transactions, no matter how minor. Small amounts can quickly sums to nig ones, leading to issues come tax season. Every hour you spend organizing your financial records now will save you many hours of stress and scrambling later. Take it one step at a time, start with the most recent records and work backward, focus on the big-ticket items first, and remember that progress always beats perfection. Catching up on months or years of neglected bookkeeping feels daunting and will require concentrated effort.