Every small business dreams of taking its business to exponential growth. While they do their best in their expertise field, they often neglect an important business aspect, and that is to keep clear and structured bookkeeping records. Bookkeeping may seem like just another task on your to-do list. But it requires a lot of your attention. It is important to consider bookkeeping records as a priority; without clear records, you will be losing track of your income, missing bill payments and being charged for delayed payments, missing out on tax benefits, and more. Poor bookkeeping just doesn’t affect your account, but it affects your business and your dreams.

In this article, we will discuss critical bookkeeping mistakes businesses should avoid. Effective financial records will help you to get sustainable growth, enabling you to make informed decisions.

Accurate books show if your business makes sense. You see money in and money out. You can spot unpaid bills, stock that isn’t selling, or costs that repeat. Good books help you know fixed costs (like rent) and variable costs (like raw materials). This helps you figure out when you’ll break even.

If you want a loan, up-to-date books are a must. No lender will give you money if you can’t prove your past income and costs. Would you trust a business that doesn’t know its profit for six months? Probably not. Investors and buyers won’t either. If you ever want to sell your business, you need clear records.

Most businesses neglect bookkeeping, often because it's very repetitive and time-consuming. However, skipping it can take your business at your business. Here's what happens when you don't keep proper books. If you can’t show good records, an audit will be stressful and expensive.

The IRS doesn't care about your excuses. They want accurate tax returns. Without good records, you can't prove your expenses or income. When you get audited, missing records mean you lose. The IRS will estimate your income high and throw out your deductions. You'll pay way more than you should. Tax penalties add up fast. Many businesses close because they can't pay the penalties - not because they weren't making money.

You won't know who owes you money. You might pay the same bill twice. You'll miss early payment discounts that could save you thousands. Without records, you can't see cash flow patterns. You won't know when busy seasons are coming or when things slow down. This leaves you scrambling when you need cash.

Every business needs money at some point. Banks want to see clean financial records before they lend. No books means no loan. This goes for investors too. They want proof your business works. Equipment financing and supplier credit - they all need financial documentation.

You can not manage what you don't measure. Without good books, you won't know which products make money and which lose money. You might spend time on things that don't pay. You might price things wrong. You might hire a bookkeeper when you should cut costs or cut when you should grow. Many business owners are shocked when they see the actual number, they finally see their real numbers. The products they thought were winners were losers.

5. Legal Problems

When customers or suppliers dispute charges, you need proof. Without records, you can't prove you paid bills or that customers owe you money.This means you'll settle disputes for more than you should. You might even face regulatory penalties if your industry requires certain records.

If you get audited without proper records, you're in trouble. Auditors will use estimates that favor the government. You'll pay taxes on money you didn't make.The burden of proof is on you. No records mean you can't prove anything.

You can do taxes without good books, but it’s a headache. You’ll spend days digging through old papers. That’s time better spent on your business. Your accountant will also need more time, which costs more money. It’s cheaper to keep books up to date all year.

8. IRS Penalties

If the IRS checks your records, they expect clear proof. If you can’t show it, you risk fees and penalties.

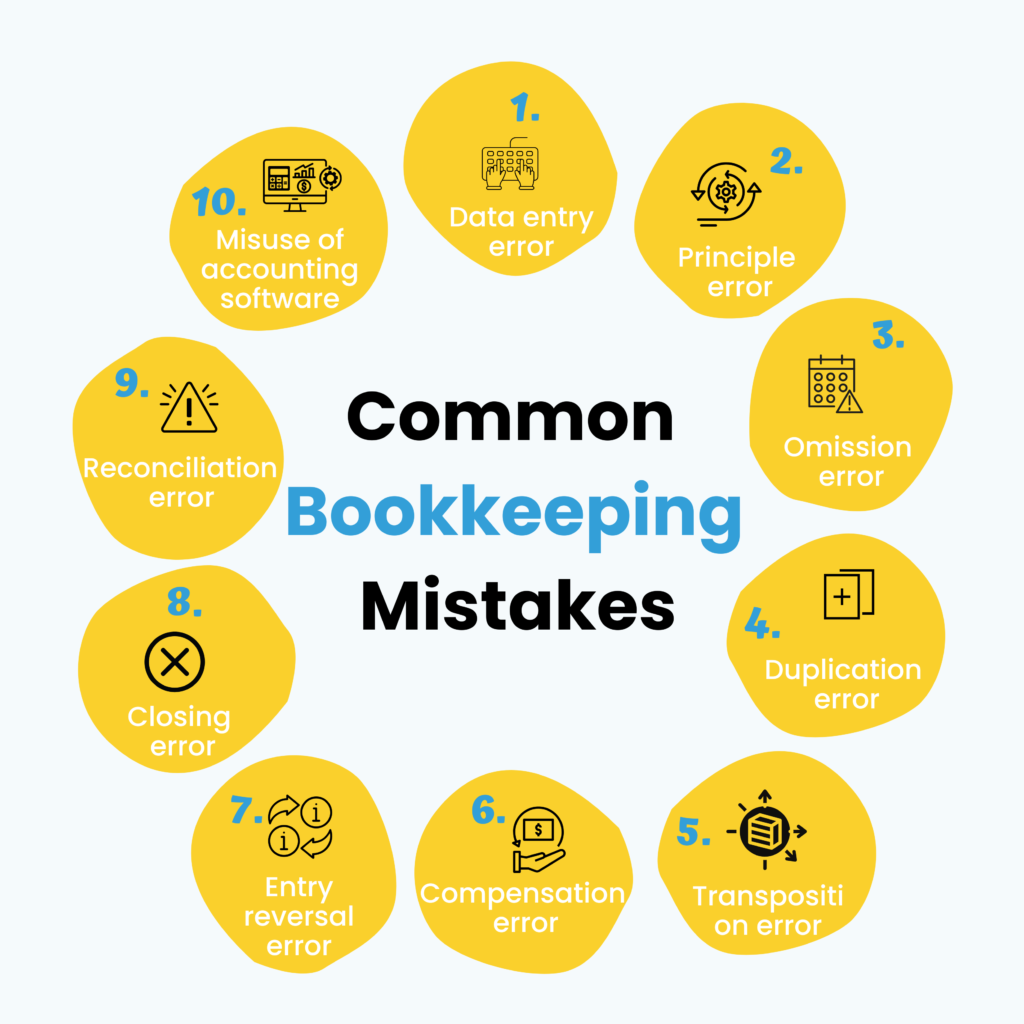

Critical errors in the IRS include the following:

Good bookkeeping isn’t hard, but it’s easy to ignore. Do a little each week and you’ll stay ahead.

Use simple software like QuickBooks, Xero, or a spreadsheet. Start small and upgrade if you need to.

Use four main buckets: income, expenses, assets, and liabilities. Don’t add extras until you need them.

Enter transactions as they happen. Use your phone to snap receipts and save time.

Pick one day a week to update your books. Block 30 minutes on your calendar.

Use a separate bank account and card for business. This makes tracking clean and clear.

Save receipts for every expense. Take photos and back them up to the cloud.

Review your books once a month. Make sure income, expenses, and bank balances match.

Set aside 25–30% of profit for taxes. Keep tax papers in one place.

Hire a bookkeeper if you’re growing fast or keep making mistakes. They cost less than fixing errors later.

Keep your personal assets and business money separate. Check even the smallest transactions.

Good books keep your business strong. They help you handle cash, get loans, and avoid tax problems. You can do it yourself or choose us for your bookkeeping solutions. The choice is yours, but the need isn't optional. Every day you wait makes the problem bigger. Start keeping good records today—your business depends on it.