You’re talented and ambitious but launching a small business doesn’t automatically make you a finance expert. Understanding Accounting 101 is essential for every business owner because it can save you both time and money in the long run. Whether you excel at numbers or prefer a more creative approach, knowing the fundamentals of accounting is crucial. Every entrepreneur needs to be aware of their business’s financial health and grasp the basics of accounting to make informed decisions and ensure success

What is accounting?

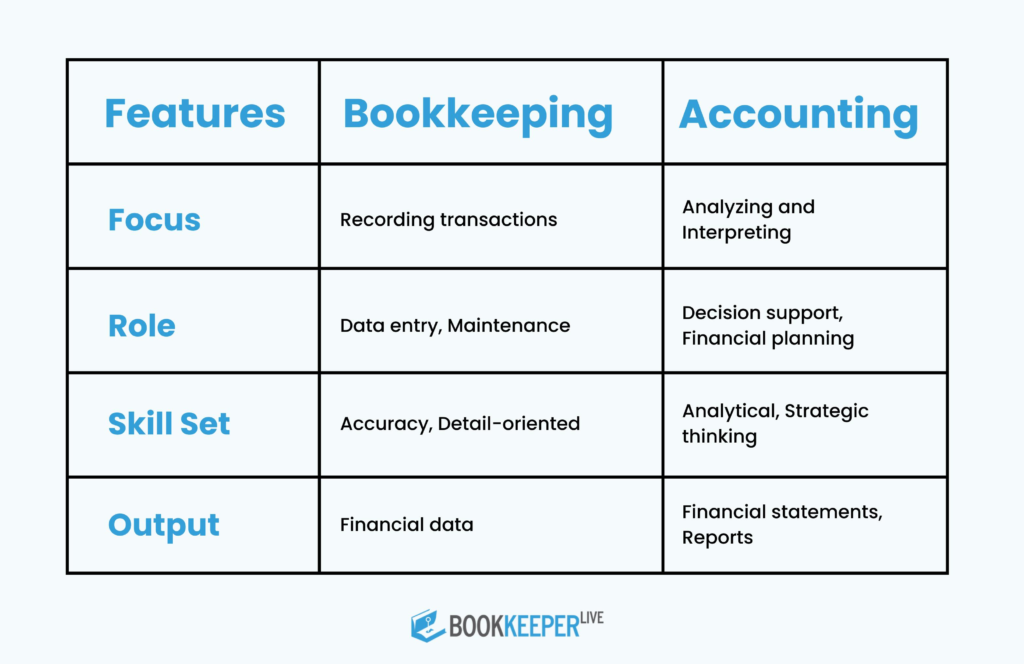

Accounting is a structured method for recording, classifying, summarizing, analyzing, and interpreting financial transactions to give a clear view of a business's financial status. It involves tracking income, expenses, and cash flow, preparing financial statements, and using this data to make informed decisions about the business's performance and future. In essence, accounting acts as the language of business, delivering essential insights to owners, investors, creditors, and management.

What is business accounting?

Business accounting involves both bookkeeping and managerial accounting to oversee a company's daily financial operations and set long-term financial goals. It encompasses activities such as forecasting, invoicing, financial tracking, analysis, recordkeeping, and budgeting. Business accounting plays a crucial role in both strategic decision-making and detailed operational management.

Typically, business accounting is more relevant for smaller businesses rather than large corporations. Small businesses may choose to handle their accounting in-house or partner with an accounting firm, depending on their size and needs. The core focus of business accounting is management, with key tasks aimed at monitoring cash flow, expenses, and inventory to ensure financial health and stability.

What do accountants actually do?

Accountants are responsible for managing a business's financial records and ensuring that all data is accurate. They use this information to prepare budgets, generate financial reports, and create essential documents. Their role involves monitoring incoming revenue and aligning it with necessary expenses to keep the business running smoothly. Additionally, accountants handle compliance with financial regulations to avoid legal issues.

Beyond these tasks, accountants often analyze cash flow statements to evaluate operations or review income statements in preparation for board meetings. They may also participate in meetings to provide financial advice and insights. Common duties include:

- Gathering new financial data and updating existing records. - Collecting documentation for audits and legal matters. - Calculating taxes and ensuring timely payments. - Verifying adherence to relevant laws and regulations. - Forecasting financial trends and assessing potential risks.

These activities help maintain financial accuracy and support informed decision-making within the business.

Types of accounting

Tax season might be a headache for some, but for tax accountants, it's their bread and butter. They navigate the complexities of tax codes, ensuring your business complies with federal and state regulations. From filing yearly returns to tracking expenses and assisting employees with tax forms, they keep your business on the right side of the IRS.

1.Financial accounting: Masters of the balance sheet

Financial accountants are all about the company's financial health. They meticulously track assets and liabilities, ensuring your accounting practices follow Generally Accepted Accounting Principles (GAAP) – a set of standardized rules for financial reporting. They work with cash flow statements and balance sheets, painting a clear picture of your company's financial position for external stakeholders like investors and creditors.

2. Management accounting: Strategists with numbers

Management accountants are the financial data whisperers. They translate complex financial information into insights for internal stakeholders and senior leadership. They play a crucial role in analyzing which products or services are profitable and how to best finance these endeavors. Think of them as financial consultants who help guide your business strategy.

3. Forensic accounting: The financial detectives

Forensic accounting involves a meticulous investigation and analysis of financial information for businesses. Much like detectives, forensic accountants delve into financial records to identify compliance breaches or illegal activities. They utilize their expertise to audit organizations, uncovering financial misconduct and ensuring adherence to legal and regulatory standards.

4. Cost accounting: Expense elimination experts

Cost accountants maintain a detailed record of all business expenses. This information helps track spending and manage costs more effectively. They identify redundancies and opportunities to reduce expenses, improving overall financial efficiency.

5. Auditing: Guardians of financial accuracy

Auditors are accountants who focus on examining financial documents to ensure they adhere to tax laws, regulations, and accounting standards. They assess organizations' financial records to verify accuracy and compliance with legal requirements.

6. International accounting: The global financial navigators

For businesses expanding internationally, international accounting is essential. These specialized accountants are well-versed in trade laws, foreign currency exchange rates, and the accounting practices of various countries. They manage the complexities of global operations to ensure seamless financial transactions and compliance across borders.

Remember, choosing the right accounting specialty depends on your specific needs. As your business grows, so might its accounting requirements. This blog provides a roadmap to navigate the diverse world of accounting and find the perfect financial partner for your entrepreneurial journey.

Accounting skills

Successful accountants bring a diverse set of skills to their role, each critical for maintaining accurate financial records and making informed business decisions. Here’s a detailed look at the key skills essential for effective accounting:

Analytical skills

Data interpretation: Accountants analyze financial data to understand trends, identify patterns, and detect anomalies. This analysis helps in forecasting future financial performance and making data-driven decisions.

Insight generation: They use analytical skills to uncover opportunities for cost savings, revenue enhancement, and overall financial improvement, providing valuable insights for strategic planning.

Communication skills

Clear reporting: Accountants must effectively communicate financial information to stakeholders, including those without a financial background. This involves simplifying complex data into understandable reports and presentations.

Advice and recommendations: They need to articulate financial findings and recommendations clearly, helping business owners and managers make informed decisions based on the data provided.

Organizational skills

Systematic record-keeping: Keeping financial records well-organized is essential for easy retrieval and review. Accountants must ensure that documents are systematically filed and accessible for audits, reviews, and daily operations.

Efficient workflow management: They manage various financial documents and reports, ensuring that everything is up-to-date and correctly archived, which helps streamline processes and enhances efficiency.

Technical proficiency

Software utilization: Proficiency with accounting software and tools, such as QuickBooks, Excel, or other financial management systems, is crucial. Accountants use these tools to automate processes, manage data, and generate reports.

Tech adaptability: They must stay updated with advancements in technology and accounting software to leverage new features and improve the efficiency of financial management.

Problem-solving abilities

Issue resolution: Accountants must address and resolve financial discrepancies, issues, and challenges effectively. This involves investigating the root cause of problems and implementing appropriate solutions.

Creative solutions: They need to think critically and develop creative solutions to overcome financial obstacles and optimize financial processes, ensuring that the business remains compliant and financially sound.

These skills collectively enable accountants to manage financial operations efficiently, provide valuable insights, and support the overall financial health and success of the business.

Principles of accounting

Understanding and applying fundamental accounting principles is crucial for maintaining accurate financial records and ensuring transparency in business operations.

Principle of regularity

Description: Accountants must comply with established standards and regulations, specifically the Generally Accepted Accounting Principles (GAAP).

Importance: This principle ensures uniformity and fairness in financial reporting, making it possible to compare different companies on an equal footing. Without it, each company might report its financials differently, leading to confusion and potential mistrust.

Application: Adhere to all Financial Accounting Standards Board (FASB) guidelines, ensuring that all financial statements are prepared in accordance with GAAP.

Principle of consistency

Description: Financial information should be reported consistently over time.

Importance: Consistent reporting allows for reliable comparison across different periods and departments within a company. This helps in tracking performance trends and making informed decisions based on historical data.

Application: Establish clear processes for recording and reporting transactions as soon as you start your business. Once these processes are set, stick to them, and clearly state any changes in financial reporting.

Principle of sincerity

Description: Accountants should present an accurate and truthful picture of the company’s financial status.

Importance: This principle builds trust with investors and stakeholders by ensuring that the data presented is reliable and not misleading. It is a commitment to honesty and integrity in financial reporting.

Application: Maintain financial records honestly and accurately, ensuring that all data presented in financial statements reflects the true financial position of the company.

Principle of permanence of methods

Description: The methods used in financial reporting should remain consistent over time.

Importance: Consistency in methods makes it easier to compare financial records across different periods, providing a clear and accurate picture of financial performance over time.

Application: Clearly organize and maintain consistent daily bookkeeping practices. Create standardized procedures for documenting and reporting financial transactions to ensure continuity.

Principle of non-compensation:

Description: All financial data, whether positive or negative, must be reported without any expectation of performance-based compensation.

Importance: This principle ensures transparency by presenting a complete and unbiased financial picture, without any manipulation for personal gain or to present a more favorable image of the company.

Application: Create and present financial reports that are clear and accurate, disclosing all relevant information regardless of its impact on perceived performance.

Principle of prudence

Description: Financial statements should be based on factual information rather than speculation.

Importance: Provides a realistic overview of the company’s financial situation, preventing overstatement or understatement of financial risks. It ensures that financial statements are conservative and reflect actual conditions.

Application: Maintain accurate and timely records, prepare for potential losses without expecting profits prematurely, and ensure that all financial data is based on verified information.

Principle of continuity

Description: Assumes that the business will continue its operations in the foreseeable future.

Importance: Helps stakeholders understand and compare performance over time by focusing on ongoing operations. It also ensures that financial statements are prepared with a long-term perspective in mind.

Application: Maintain consistent processes for financial reporting and record-keeping, even as the business plans and implements changes.

Principle of periodicity

Description: Financial entries should be reported within the appropriate time periods.

Importance: Facilitates understanding and comparison of financial performance over regular intervals. This helps stakeholders assess the company’s performance in a timely and accurate manner.

Application: Report finances annually, quarterly, and monthly. Establish a clear fiscal year from the outset of your business and adhere to these reporting periods consistently.

Principle of materiality

Description: Important financial and accounting data should be fully disclosed in financial reports.

Importance: Ensures that all significant information is available to stakeholders, while less critical details can be omitted. This allows stakeholders to make informed decisions based on the most relevant information.

Application: Start by recording every transaction, then refine the process to focus on material transactions as the business grows. Regularly review what constitutes a material transaction and adjust your reporting practices accordingly.

Principle of utmost good faith

Description: Parties involved in transactions should remain honest and transparent.

Importance: This principle establishes trust and ensures that all relevant information is disclosed before agreements are made. It reinforces the commitment to honesty and transparency in all business dealings.

Application: Be forthright in sharing crucial financial details with stakeholders before finalizing any contracts, ensuring that all parties have a clear and complete picture of the company’s financial situation.

By adhering to these principles, businesses can ensure that their financial practices are transparent, consistent, and trustworthy. This fosters confidence among investors, stakeholders, and regulatory bodies, ultimately contributing to the long-term success and sustainability of the business.

Basic accounting terms in detail

Understanding these basic accounting terms is crucial for making informed decisions about your business finances. Here's a detailed explanation of each term:

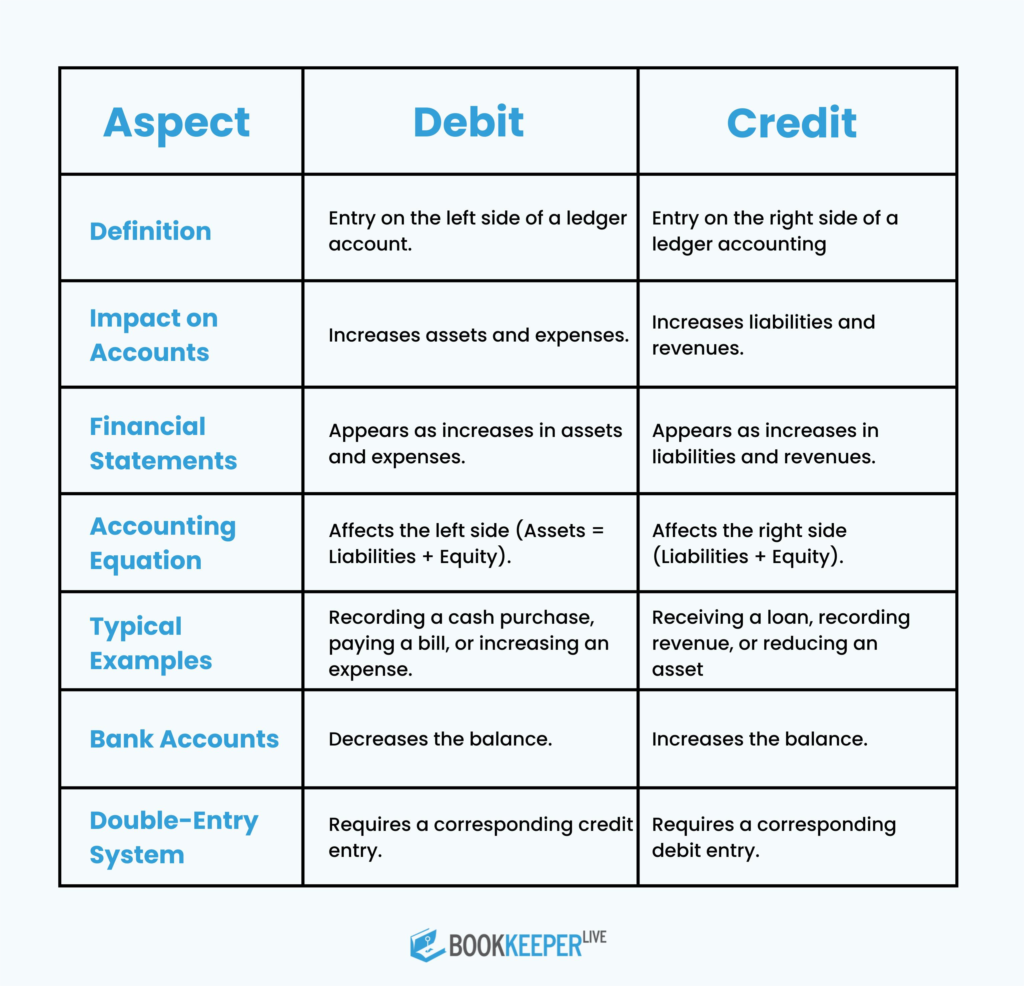

1.Debits & Credits

Debits: Represent money expected to come into an account. In double-entry accounting, debits increase asset or expense accounts and decrease liability, equity, or revenue accounts.

Credits: Represent money expected to leave an account. Credits decrease asset or expense accounts and increase liability, equity, or revenue accounts.

Example: If you pay for office supplies with cash, your cash account is credited (decreased), and your office supplies expense account is debited (increased).

2. Accounts receivable & Accounts payable

Accounts receivable (AR): Money owed to you by customers for goods or services delivered on credit. It's recorded as an asset on the balance sheet.

Accounts payable (AP): Money your business owes to suppliers or vendors for goods or services received. It's recorded as a liability on the balance sheet.

Example: If you sell products worth $10,000 on credit, your AR increases by $10,000. When you purchase raw materials worth $5,000 on credit, your AP increases by $5,000.

3. Accruals

Accruals: Revenues and expenses that are recorded when they are earned or incurred, not when cash is exchanged. This aligns with the accrual basis of accounting, providing a more accurate financial picture.

Example: You deliver a service in December but receive payment in January. Under accrual accounting, the revenue is recorded in December.

4. Assets

Assets: Resources owned by your business that have economic value and can provide future benefits. They can be tangible (physical items) or intangible (non-physical items).

Example: Tangible assets include machinery, buildings, and inventory. Intangible assets include patents, trademarks, and goodwill.

5. Burn rate

Burn Rate: The rate at which your business spends cash over a specific period, often used by startups to track their cash flow.

Calculation

Burn Rate= Starting Cash−Ending Cash divided by Number of Months

Example: If your starting cash is $50,000 and ending cash is $30,000 over 2 months, the burn rate is $10,000 per month.

6. Capital

Capital: Funds available to invest in and grow your business. It can be in the form of cash, equipment, or other resources.

Example: Working capital includes cash on hand, accounts receivable, and inventory that can be used to fund day-to-day operations.

7. Cost of goods sold (COGS)

COGS: The direct costs of producing the goods sold by a company, including materials, labor, and manufacturing overhead.

Example: If you sell handmade furniture, your COGS would include the cost of wood, labor for assembly, and any other direct costs.

8. Depreciation

Depreciation: The systematic allocation of the cost of a tangible asset over its useful life. This reflects the asset’s decreasing value over time.

Example: If you purchase a vehicle for $30,000 with a useful life of 5 years, annual depreciation using the straight-line method would be $6,000.

9. Equity

Equity: The residual interest in the assets of the business after deducting liabilities. It represents the owner’s stake in the company.

Example: If your business has $100,000 in assets and $40,000 in liabilities, the equity is $60,000.

10. Expenses

Expenses: The costs incurred in the process of earning revenue. They are categorized as fixed, variable, accrued, or operating expenses.

Types

Fixed expenses: Regular, consistent costs such as rent or salaries.

Variable expenses: Costs that fluctuate with business activity, like raw materials.

Accrued expenses: Expenses that have been incurred but not yet paid.

Operating expenses: Necessary costs to run the business, like utilities and office supplies.

Example: Monthly rent of $2,000 is a fixed expense, while the cost of raw materials used in production is a variable expense.

11. Fiscal year

Fiscal year: A one-year period that companies use for accounting purposes. It may or may not align with the calendar year.

Example: A company might choose a fiscal year from April 1 to March 31, rather than the calendar year from January 1 to December 31.

12. Liabilities

Liabilities: Financial obligations or debts owed by the business to outside parties. They can be short-term (current liabilities) or long-term.

Example: Short-term liabilities include accounts payable and taxes payable, while long-term liabilities include loans and mortgage obligations.

13. Profit

Profit: The financial gain after deducting expenses from revenue. It’s a measure of the business’s financial success.

Example: If your revenue is $150,000 and your total expenses are $100,000, your profit is $50,000.

14. Revenue

Revenue: The total income generated from the sale of goods or services before any expenses are deducted.

Example: If you sell products worth $200,000 in a year, that amount is your revenue.

15. Gross margin

Gross margin: The difference between revenue and the cost of goods sold (COGS), indicating the efficiency of production and sales.

Example: If your revenue is $500,000 and COGS is $200,000, your gross margin is $300,000.

These terms form the foundation of accounting knowledge, enabling you to better manage and understand your business finances.

Conclusion

Understanding the fundamentals of accounting is crucial for every business owner, regardless of their financial background. By grasping the core principles, terms, and skills involved, you can make informed decisions, manage your finances effectively, and ensure your business's financial health.

While managing your own accounting can be rewarding, it can also be time-consuming. Consider outsourcing your accounting needs to a professional service. Outsourced accounting services can provide expertise, efficiency, and compliance, allowing you to focus on growing your business.

By investing time in learning accounting basics or partnering with accounting professionals, you're taking a significant step towards financial success. Remember, a strong financial foundation is essential for building a thriving business.

What's Bookkeeper?

BookkeeperLive provides affordable bookkeeping and accounting services tailored to your business goals.